How to Launch an ATM Business: Earning Up to $1,500 Monthly - Side Hustle Nation

Side Hustle Nation is focused on enhancing your personal profitability. To achieve this, we frequently collaborate with companies that have a similar goal. If you register or make a purchase via one of our partners' links, we might receive compensation—without any additional cost to you. Find out more.

What if you could generate $1,500 a month in side income with just one hour of work each week — through a business that nearly operates on its own?

This is precisely what Will Butterton has accomplished with five ATMs via his company, Viking Vendors LLC.

Will is a full-time engineer, a father of three, and a multi-side-hustler who entered the ATM business as his wife was expecting, seeking a low-risk opportunity. He started the venture with a childhood friend, both investing in their initial two machines. The proposition was straightforward: in the worst-case scenario, they could not secure locations and could sell the machines to someone else.

Catch Episode 741 of the Side Hustle Show to discover:

- What it genuinely takes to launch an ATM business from the ground up, including the unexpected challenging step.

- How to identify and pitch potential locations — even when most prime spots already have a machine.

- The financials across various types of locations, and how a single prime spot can significantly boost your income.

The Mechanics of the ATM Business

The concept is simple: you own ATMs, position them in businesses, and earn a surcharge fee with each withdrawal. This fee, typically around $3 per transaction, constitutes your total profit margin.

Will currently operates five machines generating about $1,500 a month, requiring just an hour of work each week. He shares responsibilities with his partner: his friend takes care of cash collection, while Will oversees the remainder.

However, the potential for revenue is much higher. In Washington state, a single ATM in a dispensary can process over $5,000 in cash daily. With 25 transactions per day over a month at a $3 surcharge, that could lead to $2,250 a month from just one location—more than Will earns from all five machines combined.

Step 1: Establish Your LLC and Open a Business Bank Account

Before making any purchases, you must establish your LLC and obtain an EIN (your federal tax number). This portion is fairly easy.

What’s more challenging is opening a business bank account. Major national banks ceased working with ATM operators following a federal investigation in the early 2010s linking ATMs to money laundering and organized crime. This resulted in a blanket policy making it difficult for legitimate operators.

Will had to contact 6 or 7 local banks before he found one willing to assist him. His recommendation is to start with local banks and credit unions, choosing one with sufficient branches near your locations to avoid long drives whenever you need to withdraw cash. He views this as the most challenging task in starting the business.

Step 2: Purchase Your Machines

Plan to budget around $4,500 per machine to kick things off:

- $3,000 for the ATM itself (Will prefers the Genmega 2500; Hyosung machines are also good).

- $1,000+ in cash to load the machine.

- $500 for receipt paper, parts, and other supplies.

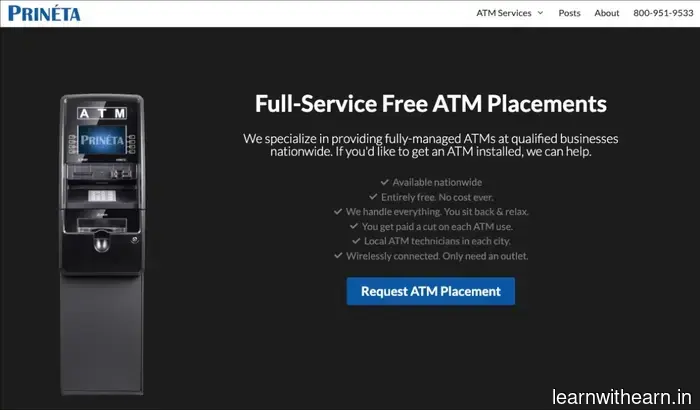

Will acquires his machines from Prineta, the same company that processes his transactions, which simplifies the setup process.

Step 3: Select the Right ATM Processor

Your financial outcome hinges on the surcharge fee, making this more critical than it appears. Ensure you find a processor that takes 0% of your surcharge. Some charge 10%, which may seem minor but adds up quickly.

Will uses and recommends Prineta for this purpose as they don’t take any portion of his surcharge—if he charges $3, he receives the full $3. Their customer service is also highly responsive: you can text them directly and receive a prompt reply. Processors earn from backend agreements with card networks, not from your fee.

Another banking tip: Will operates three separate bank accounts for:

- Vault cash – the funds you load into machines.

- Incoming transactions – where the surcharge fees are deposited.

- Savings buffer – for slow periods or unexpected expenses.

Step 4: Find and Secure Locations

This phase involves significant effort. Most prime locations already have an ATM, so your pitch typically isn’t ‘you need this’ but rather ‘I’ll provide a better service.’

The most common feedback Will receives from business owners is that their current ATM is frequently out of order and takes too long to get repaired. This situation is similar to how vending machine operators expand their side hustle.

Will's advantage is being local, providing his cell number, and guaranteeing same-day service. He also presents himself professionally—wearing a button-up shirt with his logo and dress pants—treating every pitch like a significant sales call

Other articles

How to Launch an ATM Business: Earning Up to $1,500 Monthly - Side Hustle Nation

Launch an ATM business and earn over $1,000 monthly in passive income. Discover the precise startup expenses, location strategies, and ways to overcome banking obstacles.